Third Quarter 2025 Quarterly Market Update: Riding the Wave

October 7, 2025 | Market Updates

GreenUp Wealth Management reviews Q3 2025 market trends, including Fed policy, consumer strength, earnings growth, high valuations, and portfolio updates.

Introduction: Riding the Economic Wave

As a child growing up in landlocked Ohio, learning to surf was a distant dream, blocked by geography, but never by desire. The metaphor is apt for today’s financial markets. Like ocean waves, economic cycles ebb and flow with undeniable momentum, propelling asset prices to impressive heights. To the naked eye, one may notice waves individually; seeing each wave’s unique phases and momentum. Yet, waves, like economies and markets, are caught in a continuous cycle of cresting and crashing, exhibiting patterns and interconnectivity; an essential step if you choose to ride the economic wave.

Our analysis of the first half of 2025 confirms we are in a mid-to-late-cycle bull market: a period of sustained economic strength where stock values rise meaningfully. For many investors, the primary concern is that bull markets often end in recessions. However, a recession is not on GreenUp Wealth’s radar for the next 12–18 months. Instead, our current economic wave is fueled by robust tailwinds: supportive government policies, a resilient consumer, and robust corporate earnings.

The Underlying Currents: Monetary and Fiscal Policy

The strategic actions of the Federal Reserve and U.S. government are the foundations of market activity. Much like deep ocean currents shaping the waves above, monetary and fiscal policies may not always drive immediate growth or contraction, but they profoundly influence the environment, including borrowing costs for consumers and businesses. Let’s examine how these policies are building momentum in our economic wave.

The Federal Reserve’s Accommodative Stance

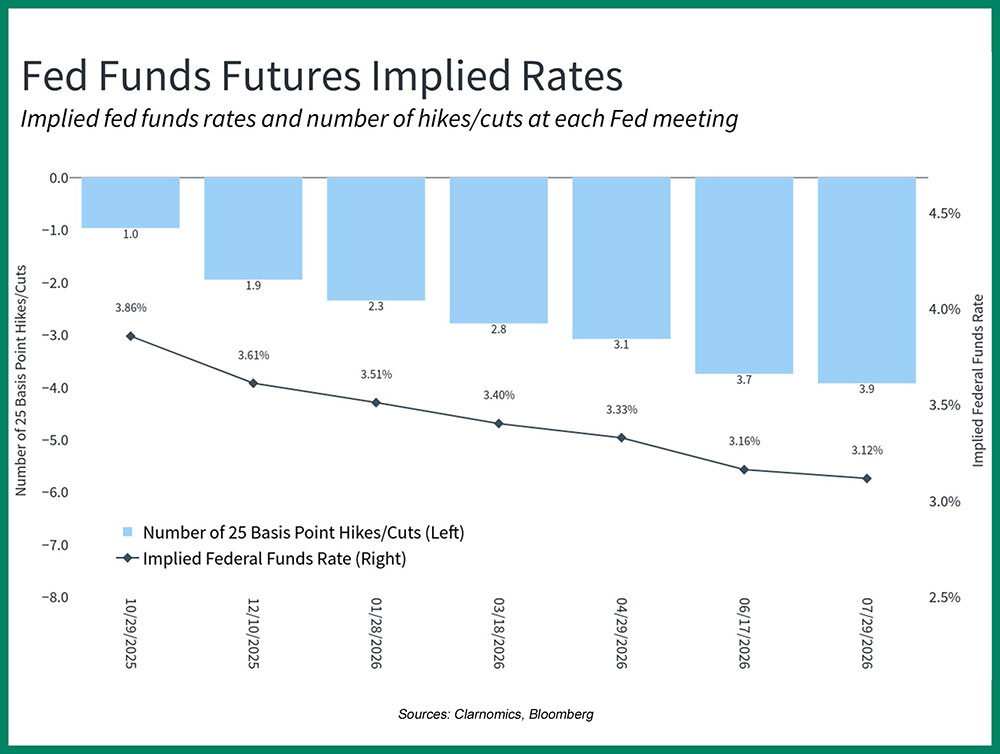

Monetary policy (where the Federal Reserve controls the amount of money in our system) remains supportive of the markets, often characterized as “dovish.” The Federal Reserve has resumed lowering interest rates, which directly benefits borrowers on everything from car loans to mortgages. Despite inflation lingering slightly above the Fed’s target of 2%, the central bank has signaled its commitment to providing liquidity and stimulating growth. Many forecasts suggested tariffs might trigger an immediate inflation spike, but that hasn’t materialized. Instead, we anticipate a more gradual impact, potentially elevating inflation by 0.1–0.2% per measure over time.

This policy fosters market liquidity and reflects the Fed’s tolerance for modestly elevated inflation, encouraging investment and lending. That said, persistent “sticky” inflation could temper the pace and extent of future rate cuts.

Supportive but Unpredictable Government Spending

On the fiscal side, government spending continues unabated. The recent passage of the congressional budget in Q2 2025 suggests an end to austerity measures. Projections for the “One Big Beautiful Bill” vary widely, from potential savings of $1.7 trillion to adding $1.6 trillion to $5.3 trillion to the deficit over the next decade. In the short term, this return to deficit spending, where outflows exceed revenues, is inherently stimulative, injecting vitality into the economy and sustaining our wave’s momentum.

The Resilient U.S. Consumer

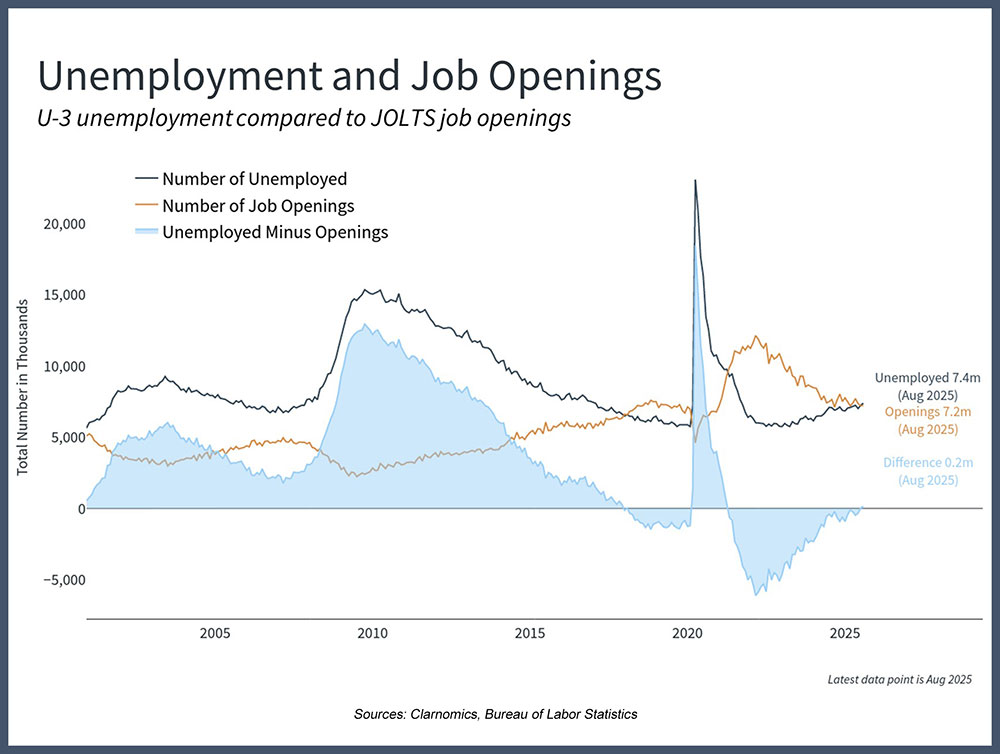

The U.S. consumer remains a powerhouse, and continues to drive economic growth, thanks to a solid job market and real wage gains. Like monetary and fiscal policies (the Federal Government tax and spending policy), consumer behavior is extending the life of our economic wave. Since 2020, employers have fueled a hiring boom to meet demand. Job openings peaked at 12.18 million in February 2022 and have since moderated to a still-robust 7.1 million. That equates to about 0.9 openings per job seeker. With unemployment hovering at 4.3%, the labor market appears healthy at this time.

However, beneath the surface, dynamics are shifting in favor of employers. A 4.3% unemployment rate is hardly cause for alarm – jobs remain plentiful, but the tides could be turning. Artificial Intelligence (AI) is delivering on its promise. At GreenUp Wealth, we’re enthusiastic about AI’s potential to streamline scheduling, enhance productivity, and even introduce helper robots within 5–7 years. But there’s a caveat: AI equips workers with vast knowledge while displacing certain roles. This is beginning to unfold in the labor market.

In September 2025, a major revision revealed that job growth over the prior 12 months was overstated by 911,000 positions – a significant adjustment. Meanwhile, recent college graduates are facing higher unemployment rates than their non-college-educated peers in the same age group. We’re monitoring these trends closely, but they haven’t yet signaled a threat to broader growth. That said, we’ll keep a sharper eye on the labor market over the next 12 months to ensure these cracks don’t widen.

Our optimism for the consumer is bolstered by wage growth outpacing inflation. This signals that employers continue to value their workforce, even as hiring slows and efficiency efforts intensify. Average U.S. worker compensation is rising 4.3%, compared to 2.7% inflation – a meaningful gap that boosts purchasing power. This means even with increased costs, people have more money in their pockets to spend.

This data affirms the consumer’s strength: rising incomes, growing wealth, and sustained spending. However, softening job trends and moderating spending growth merit ongoing vigilance.

Corporate Earnings Continue to Sizzle

While policy and labor set the stage, corporate performance is the true engine of the economy. The exceptional strength of U.S. companies, paired with the resilient consumer, has driven markets to new peaks. These fundamentals provide the core propulsion for our current wave.

Entering 2025, corporate profit expectations were ambitious, but tariffs prompted many analysts to lower forecasts. However, earnings have exceeded projections, which justifies and contributes to elevated equity valuations and contributing to market highs. Highlights include:

- In Q2 2025, S&P 500 earnings grew 11.7% year-over-year.

- For 2026, analysts project 15.4%–17.2% earnings growth.

This sustained double-digit growth creates a virtuous cycle, boosting investor confidence, enabling business investments, and supporting wage hikes. It’s a hallmark of this market expansion.

A Note of Caution: High Valuations

Strong economics and supportive policies have elevated market valuations to historically high levels – a natural outcome of a thriving bull market fueled by optimism. However, this also heightens risks: prices may now embed near-perfect expectations, leaving limited margin for error.

The key takeaway is that short-term volatility (over the next 3–6 months) could arise from surprises like earnings shortfalls, geopolitical events, or Fed shifts. That said, ongoing mid-teens earnings growth should limit any pullbacks to temporary corrections, which may still take 3–6 months to resolve. In essence, we’re surfing at peak height— thrilling but requiring balance.

Conclusion: This Bull Market Has Legs

Drawing from data across the first half of 2025, our thesis is unequivocal: We’re in the midst of a bull market with substantial momentum. This expansion isn’t mere speculation; it’s grounded in double-digit corporate earnings growth and a robust consumer, amplified by accommodative monetary and fiscal policies. The cycle appears poised to continue.

High valuations deserve attention, but we see them as a byproduct of genuine economic strength, not an imminent red flag. Investors should stay disciplined and cautious in expensive markets. By sticking to a tailored, long-term financial plan, you can ride this wave with confidence, navigating turbulence while focusing on your goals.

At GreenUp Wealth, we’re here to help you stay steady. Please contact your GreenUp Wealth advisor for personalized insights.

GreenUp Portfolio Updates

Dynamic/ESG Models:

New Positions: EIDOX (Eaton Vance Emerging Markets Debt Opportunities Fund), UITB (VictoryShares Core Intermediate Bond ETF), HYG (iShares iBoxx $ High Yield Corporate Bond ETF), CPEFX (Cascade Private Capital Fund)

Exited Positions: EPI (WisdomTree India Earnings Fund), AGG (iShares Core U.S. Aggregate Bond ETF), TIPWX (Bluerock Total Income + Real Estate Fund)

Equity Income Model

New Positions: KO (The Coca-Cola Co.) and UPS (United Parcel Service, Inc.)

Exited Positions: Removed FANG (Diamondback Energy, Inc.)

Large Cap Stock Model

New Positions: VEEV (Veeva Systems Inc.), BX (Blackstone Inc.), PYPL (PayPal Holdings, Inc.), QCOM (Qualcomm Inc.), ABNB (Airbnb, Inc.), AMAT (Applied Materials, Inc.), KO (The Coca-Cola Company), GILD (Gilead Sciences, Inc.), GD (General Dynamics Corp.), LLY (Eli Lilly and Company), LDOS (Leidos Holdings, Inc.), NU (Nu Holdings Ltd.)

Exited Positions: DEO (Diageo plc), COP (ConocoPhillips), XOM (Exxon Mobil Corporation), CVS (CVS Health Corporation), CMCSA (Comcast Corporation), MA (Mastercard Incorporated), KMX (CarMax, Inc.), CRM (Salesforce, Inc.), PEP (PepsiCo, Inc.), FI (Fiserv, Inc.), ELV (Elevance Health, Inc.), BRK.B (Berkshire Hathaway Inc.), SNY (Sanofi), NVS (Novartis AG), LRCX (Lam Research Corporation), JPM (JPMorgan Chase & Co.)

Tactical Equity Model

New Position: FYC (First Trust Small Cap Growth AlphaDEX Fund)

Exited Position: FXU (First Trust Utilities AlphaDEX Fund)

GreenUp Street Wealth Management, LLC d/b/a GreenUp Wealth Management is an investment advisory firm registered with the Securities and Exchange Commission (“SEC”) under the Investment Advisers Act of 1940. Registration as an investment adviser does not imply a certain level of skill or training. The oral and written communications of an adviser provide you with information about which you determine to hire or retain an adviser. Form ADV Part 2A can be obtained by visiting https://adviserinfo.sec.gov and searching for our firm name. ADV Form 2B is available upon request. Neither the information nor any opinion expressed is to be construed as solicitation to buy or sell a security or personalized investment, tax, or legal advice.

This report has been provided for informational purposes only and is not intended as legal or investment advice or a recommendation of any particular security or strategy. The investment strategy and themes discussed herein may be unsuitable for investors depending on their specific investment objectives and financial situation. Information obtained from third-party sources is believed to be reliable though its accuracy is not guaranteed. Opinions expressed in this commentary reflect subjective judgments of the author based on conditions at the time of publication and are subject to change without notice. Past performance is not indicative of future results.

Any forecasts presented in this document, including estimates of returns or performance, are “forward looking statements”, are based upon certain assumptions about future events or conditions and are intended only to illustrate hypothetical results under those assumptions, and no assurances can be made that they will materialize. Forward-looking statements are based on an assumption that economic, market, political, operational, legal, tax, regulatory and other conditions will not deteriorate and, in some cases, improve.

Definitions:

Personal Consumption Expenditure (PCE) – a measure of the prices that people living in the United States, or those buying on their behalf, pay for goods and services. The PCE price index is known for capturing inflation (or deflation) across a wide range of consumer expenses and reflecting changes in consumer behavior.

S&P 500 – measures the performance of 500 widely held stocks in US equity market. Standard and Poor’s chooses member companies for the index based on market size, liquidity and industry group representation. Included are the stocks of industrial, financial, utility, and transportation companies. Since mid-1989, this composition has been more flexible and the number of issues in each sector has varied. It is market-capitalization weighted.

Author

Daniel Greulich, CFA CFP®

Chief Investment Officer | Wealth Advisor | Ann Arbor, MI -- Daniel leads our Investment Committee and partners with Aaron Kirsch, Chief Client Advocacy Officer to design and implement client portfolios with your advisor. Daniel brings 14 years of practical experience as a trader, financial advisor, and money manager at both large and mid-sized financial services companies to GreenUp Wealth Management. In addition, he holds a CFP® designation and is also a CFA charterholder. This combination of experience and knowledge helps Dan confidently guide his clients through the development, execution and monitoring of their customized financial plans.

All Posts