Quarterly Market Update 2026 Q2

July 13, 2026 | Market Updates

Throughout the year, several structural mega-trends have emerged, acting as tides of change rolling through the economy. As investors, we must acknowledge that these waves of change—both good and bad—are inherently difficult to navigate.

The good news is that while these powerful tides are challenging different industries, they do not appear to be crashing over all industries at once. This staggered timing gives the broader economic ecosystem the space it needs to absorb the changes, adapt, and steady itself. We anticipate these structural swells will drive economic and financial analysis for years to come—frequently overshadowing short-term headline risks, such as geopolitically driven spikes in commodity prices.

These tides of change or “structural trends” currently fall into three primary categories:

- Artificial Intelligence and Corporate Earnings: The rapid integration of AI continues to act as a massive catalyst, driving outsized growth in corporate earnings.

- Consumer Resilience vs. “Sticky” Inflation: Consumer spending has remained remarkably robust, even as the market digests a sustained environment of high interest rates and persistent inflation.

- Fiscal and Monetary Policy Contradictions: A structural conflict has emerged between the Federal Reserve’s mandate to aggressively control inflation and the federal government’s continued reliance on deficit spending. While this fiscal stimulus supports the broader economy, it simultaneously fuels underlying inflationary pressures and exacerbates wealth inequality.

1. Artificial Intelligence and Corporate Earnings

Let’s start with one of the positive Tides of Change. For those wondering what is driving the market’s above-average returns, look no further than U.S. corporate profitability. 2026 has been a remarkable year as the anticipated productivity gains driven by Artificial Intelligence are finally materializing on the bottom line. While the shift may appear subtle on the surface, S&P 500 companies—representing the premier large-cap businesses in the United States—are delivering their strongest earnings growth since the 2021 reopening boom.

Before we dive into the broader macroeconomic story, it is important to ground our analysis in the staggering numbers we are currently seeing:

- Exceptional Q1 Earnings Growth: Q1 2026 S&P 500 earnings posted a 28.6% increase over trailing 12-month figures, effectively doubling the growth rate of previous quarters. These are simply phenomenal results, leading many analysts to forecast full-year 2026 earnings growth approaching 25%.

- Upward Revisions to Price Targets: Year-end forecasts for the S&P 500 are currently anchored around 7,700, with high-end estimates reaching 8,250. This implies a potential remaining upside of 2.6% to 11.5% between now and the end of the year.

- Valuation Reality and Margin Expansion: Profit margins have expanded to 14.6%, sitting well above the five-year average of 12.3%. In practical terms, these massive enterprises are retaining an additional 2.3 cents of profit for every single dollar of revenue earned. If this margin expansion is truly the result of AI-driven productivity, we expect to see this trend broaden out into mid- and small-cap equities in the coming quarters.

The primary driver behind this explosive earnings growth is the structural transition of Artificial Intelligence from a costly expense to providing tangible operational benefits. It’s working. Throughout 2024 and 2025, corporations invested heavily in tech infrastructure, a phase that many skeptics feared would depress margins and others worried would fuel a bubble. In 2026, we are witnessing the payoff: these investments have matured into enterprise software, automated workflows, and advanced analytics that are efficiency machines. AI has allowed large-cap enterprises to scale their output without a corresponding increase in costs, effectively driving outperformance in corporate earnings.

While this corporate core is remarkably robust, it does not operate in a vacuum. Ultimately, the continued strength of this expansion depends on the American consumer’s ability to ride out increasing credit strain.

2. Consumer Resilience vs. “Sticky” Inflation

“Resilient” remains the most accurate descriptor for the U.S. consumer. The sheer durability of consumer spending has solidified into a defining structural positive trend of the American economy. Over the past six years, cumulative inflation has surged by nearly 30%, and recent data suggests that a structurally “sticky” inflation rate between 3% and 4% will be difficult to break. Yet, despite these formidable headwinds, consumer spending—which accounts for roughly 70% of U.S. economic growth—continues to act as the primary engine powering the broader economy forward.

However, beneath this headline strength lies an increasingly bifurcated economy. Consumer balance sheets have seesawed dramatically from the stimulus-fueled, overflowing coffers of the pandemic era to a deeply divided reality today. As recently highlighted by Moody’s Analytics, the top 10% of income earners now account for nearly half of all consumer spending. Meanwhile, the remaining 90% of the population is struggling to keep pace with the dual pressures of elevated interest rates and persistent inflation.

From a macroeconomic perspective, the consumer appears stretched but fundamentally healthy. While several key economic conditions are currently trending negatively, it is critical to recognize that they are decelerating from historically unprecedented highs. Because the starting point was so incredibly robust, the absolute levels remain squarely in positive territory, providing a solid foundation for continued spending.

Consider the current trajectory of these key metrics:

- Wage Growth vs. Inflation: For an extended period, aggregate wage growth successfully outpaced inflation, bolstering real purchasing power for the consumer. While that dynamic has recently inverted as inflation proves sticky, baseline wages remain historically elevated, preventing a sharp contraction in spending power.

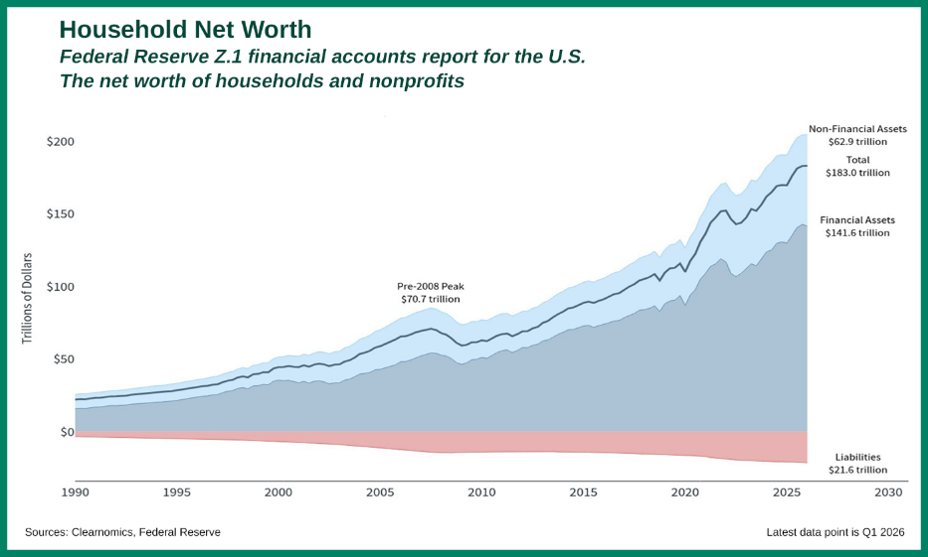

- Savings Rates vs. Household Net Worth: The personal savings rate has steadily declined as households draw down excess pandemic reserves to absorb higher day-to-day living costs. Yet, aggregate household net worth continues to climb to record highs, heavily buoyed by the “wealth effect” of appreciating equity portfolios and resilient home values.

- Hiring Volatility vs. Broad Employment: The rapid integration of AI and corporate efficiency initiatives has introduced noticeable volatility into specific sectors, creating headlines about hiring freezes and targeted layoffs. However, the broader labor market remains remarkably tight. Both the headline unemployment rate and Job Openings and Labor Turnover Survey (JOLTS) data indicate that jobs remain plentiful, providing the ultimate safety net for consumer confidence and sustained spending.

In the current economic environment, the American consumer appears remarkably resilient, with certain metrics even suggesting they are thriving. However, this headline strength creates a misleading narrative. The confusion stems from a fundamental analytical flaw: We tend to lump all consumers into a single group. In reality, we are navigating a deeply divided landscape shaped by two entirely separate consumers—those with assets and those without.

Because of this stark divide, it remains difficult to discern whether the consumer core is beginning to pull back or if these powerful, industry-challenging Tides of Change will continue to roll forward across the broader economy.

3. Fiscal and Monetary Policy Contradictions

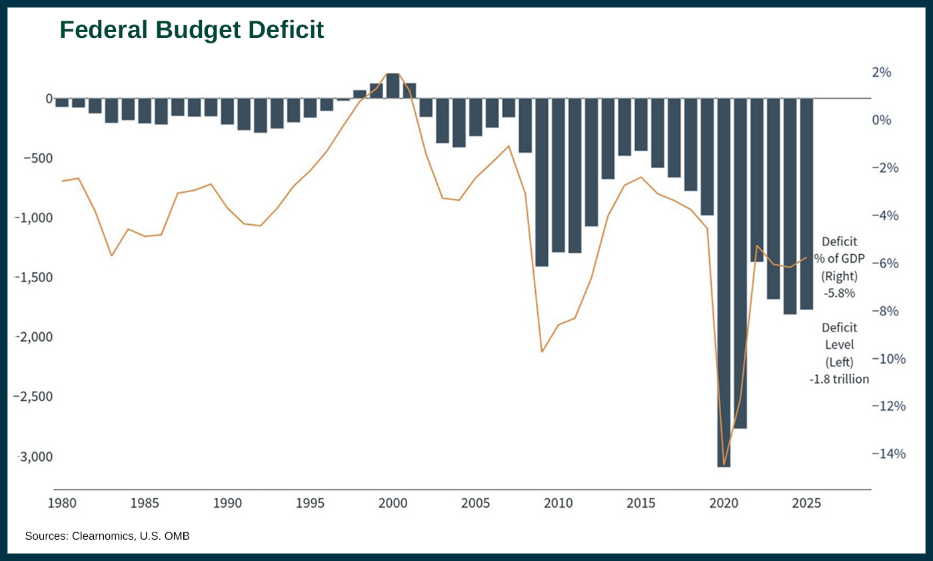

While corporate earnings and consumer spending provide a strong foundation for the economy, the macroeconomic picture is becoming increasingly complicated. We are witnessing a collision of powerful, opposing currents: on one side, the relentless wave of federal deficit spending, and on the other, the steady hand of the Federal Reserve attempting to anchor prices.

The specific tide of change we are forced to navigate is a central bank cornered by a stark compromise. The Federal Reserve must choose between two difficult paths: engineered economic deceleration to permanently break inflation, or an environment characterized by both sticky growth and sticky inflation.

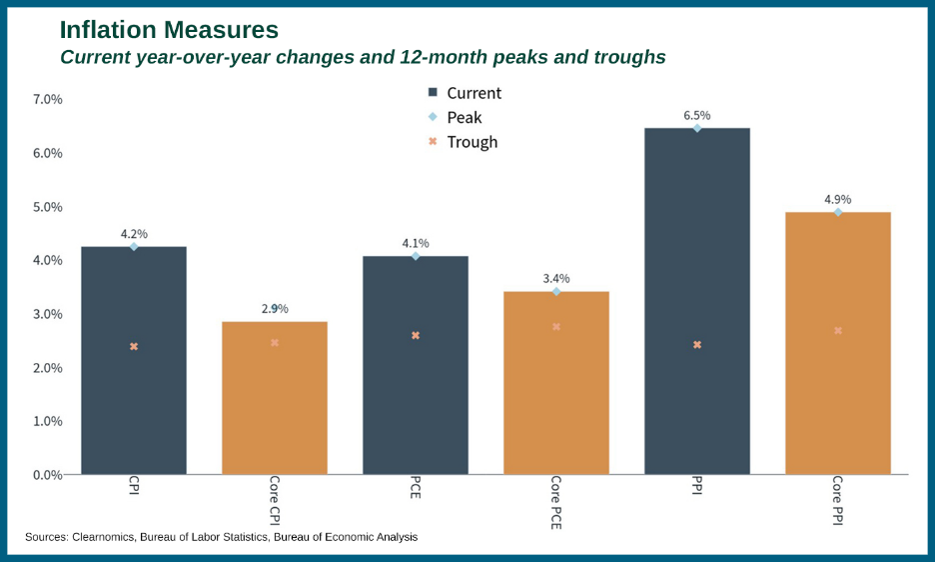

For years, investors have grown accustomed to viewing the Federal Reserve as a tailwind for asset prices and a positive force for portfolios. Moving forward, however, Fed meetings may prove to be a bit less entertaining. With inflation remaining stubbornly elevated at 4.2%, it is highly unlikely we will see interest rates decrease significantly anytime soon. Ultimately, years of unprecedented structural deficit spending have become the primary driver of the persistently sticky inflation we see today—a corrosive force that continues to eat away at both investor returns and consumer purchasing power.

On the fiscal side, the federal government continues to run massive deficits, effectively injecting capital into the system and permanently increasing the money supply chasing a finite amount of goods. Conversely, the Federal Reserve operates under an independent mandate to maintain stable prices and maximum employment. While the employment picture remains stable, inflation is running hot at 4.2%—well above the Fed’s 2% target.

Consequently, the central bank is severely constrained in its ability to cut interest rates and provide relief to an increasingly stretched consumer. This creates a challenging negative feedback loop: As consumer stress builds, the federal government is incentivized to maintain deficit spending, which in turn fuels the very inflation the Fed is trying to suppress, ultimately forcing interest rates to stay higher for longer.

Ultimately, years of unprecedented structural deficit spending have become the primary driver of the persistently sticky inflation we see today—a corrosive force that continues to eat away at both investor returns and consumer purchasing power.

Navigating the Path Forward

The critical question moving into the second half of the year is which of these Tides of Change will ultimately prevail: Will federal deficit spending trigger an inflation-fueled recession, or will the resilience of the consumer and corporate profitability continue to outpace inflationary pressures?

At GreenUp Wealth Management, we remain cautiously optimistic that corporate and consumer strength will lead the way as they have in the past. However, successfully navigating a market characterized by both high corporate profits and persistent inflation requires acknowledging two fundamental realities:

- Heightened Market Volatility: As borrowing costs remain elevated, companies will increasingly be forced to choose between funding future growth and servicing their existing debt burdens. This tension will naturally inject more volatility into the broader markets.

- The Necessity of Equity Exposure: Inflationary forces compel investors to maintain, if not increase, their equity exposure. Equities remain one of the most effective vehicles for outpacing the erosive effects of long-term inflation.

Given the necessity of maintaining stock exposure to combat inflation, our strategic approach centers on broadening diversification across both asset allocation models and individual security selection.

- Within Our Asset Allocation Portfolios, we continue to mitigate risk by balancing our core focus on large-cap domestic equities with strategic allocations to mid- and small-cap U.S. companies. We pair this domestic foundation with a balanced weighting to international equities, capturing opportunities across both developed and emerging markets to build a robust, inflation-resistant portfolio.

- For Individual Securities, we are strategically rotating away from the top-heavy, highly concentrated segments of the U.S. market. Instead, we are focusing on established businesses positioned to successfully integrate and monetize AI to drive immediate profitability, rather than strictly investing in the creators of the AI infrastructure itself.

While the intersection of these mega-trends-AI-driven margin expansion, a bifurcated consumer base, and conflicting government policies-will undoubtedly create moments of market turbulence, the underlying economic foundation remains solid. By looking past short-term headline noise and anchoring our strategies in these long-term structural realities, we are well-positioned to protect purchasing power and capture growth.

As always, our commitment at GreenUp Wealth Management is to navigate this complexity with discipline, ensuring your portfolio remains aligned with both current market dynamics and your long-term financial goals.

GreenUp Portfolio Updates

Dynamic/ESG/Index Models:

- New Positions: No new positions

- Exited Positions: No exited positions

Equity Income Model:

- No Changes

Large Cap Stock Model:

- New Positions: Exxon Mobil Corporation (XOM), General Electric Company (GE), Lam Research Corporation (LRCX), Intuitive Surgical, Inc. (ISRG), McKesson Corporation (MCK), Walmart Inc. (WMT), RTX Corporation (RTX), Salesforce, Inc. (CRM), Comcast Corporation (CMCSA)

- Exited Positions: Visa (V), Elevance Health Inc. (ELV), Mastercard Incorporated (MA), Medtronic PLC (MDT), Autodesk, Inc. (ADSK), Valero Energy Corporation (VLO)

Tactical Equity Model:

- New Position: First Trust Technology AlphaDEX Fund (FXL)

- Exited Position: First Trust Energy AlphaDEX Fund (FXN)

GreenUp Street Wealth Management, LLC d/b/a GreenUp Wealth Management is an investment advisory firm registered with the Securities and Exchange Commission (“SEC”) under the Investment Advisers Act of 1940. Registration as an investment adviser does not imply a certain level of skill or training. The oral and written communications of an adviser provide you with information about which you determine to hire or retain an adviser. Form ADV Part 2A can be obtained by visiting https://adviserinfo.sec.gov and searching for our firm name. ADV Form 2B is available upon request. Neither the information nor any opinion expressed is to be construed as solicitation to buy or sell a security or personalized investment, tax, or legal advice.

This report has been provided for informational purposes only and is not intended as legal or investment advice or a recommendation of any particular security or strategy. The investment strategy and themes discussed herein may be unsuitable for investors depending on their specific investment objectives and financial situation. Information obtained from third-party sources is believed to be reliable though its accuracy is not guaranteed. Opinions expressed in this commentary reflect subjective judgments of the author based on conditions at the time of publication and are subject to change without notice. Past performance is not indicative of future results.

Any forecasts presented in this document, including estimates of returns or performance, are “forward looking statements”, are based upon certain assumptions about future events or conditions and are intended only to illustrate hypothetical results under those assumptions, and no assurances can be made that they will materialize. Forward-looking statements are based on an assumption that economic, market, political, operational, legal, tax, regulatory and other conditions will not deteriorate and, in some cases, improve.

Author

Daniel Greulich, CFA CFP®

Chief Investment Officer | Wealth Advisor | Ann Arbor, MI -- Daniel leads our Investment Committee and partners with Aaron Kirsch, Chief Client Advocacy Officer to design and implement client portfolios with your advisor. Daniel brings 14 years of practical experience as a trader, financial advisor, and money manager at both large and mid-sized financial services companies to GreenUp Wealth Management. In addition, he holds a CFP® designation and is also a CFA charterholder. This combination of experience and knowledge helps Dan confidently guide his clients through the development, execution and monitoring of their customized financial plans.

All Posts