Second Quarter 2025 Quarterly Market Update: Push, Pull … and Opportunity

July 10, 2025 | Market Updates

The second quarter of 2025 was marked by a fierce tug-of-war in financial markets, driven by a confluence of negative forces stemming from policy uncertainty causing the S&P 500 to fall close to 20% from all-time highs.

This volatility was intensified by conflicting signals and uncertainty from the Federal Government and the Federal Reserve. As this situation developed further, economic readings on the consumer and corporate profits pulled the S&P 500 back into positive territory for the year. This “push and pull” will likely continue through 2025. The resulting market turbulence is a result of the challenges of navigating an unpredictable economic landscape.

Make no mistake about it: federal and monetary policies are driving volatility

Historical trends demonstrate that ambiguity in federal spending, lending rates, or trade agreements consistently unsettle markets. Today’s market is no exception.

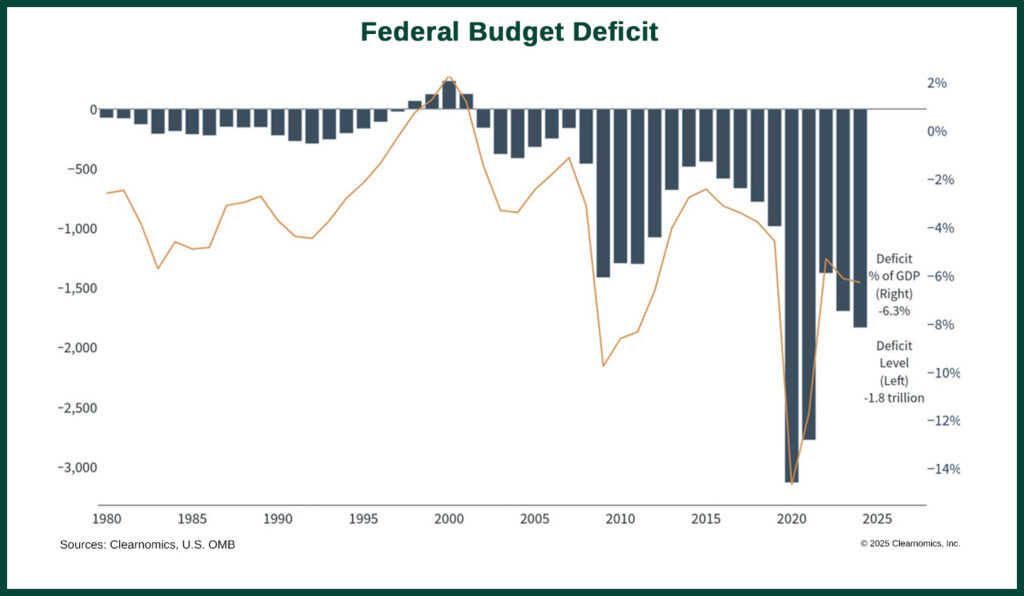

The introduction of Liberation Day tariffs introduced unease, interrupting potential new trade agreements and causing supply chain disruptions. At the same time, the Trump administration’s conflicting budget agendas are deepening this uncertainty — it’s not clear how the Department of Government Efficiency (DOGE)’s widespread layoffs square with the Big Beautiful Bill, which forecasts deficits ranging from $1.6 billion to $5.3 trillion over the next decade. Typically, the stock market celebrates more government spending, but this abrupt policy reversal left markets reeling from the whiplash of contradictory fiscal signals.

Interest rates are also dampening economic growth — even though the Fed is doing its job

The blame for this volatility doesn’t lie solely at the door of federal policy – the Federal Reserve is also compounding these challenges through inaction on interest rates, in particular.

As a reminder, the Federal Reserve is the head of our banking system in the USA, and their mandate is two-fold: to maintain a healthy level for both inflation and employment. If inflation is tamed and employment is full, one would expect a healthy banking system and thus the economy. This is a formula that works.

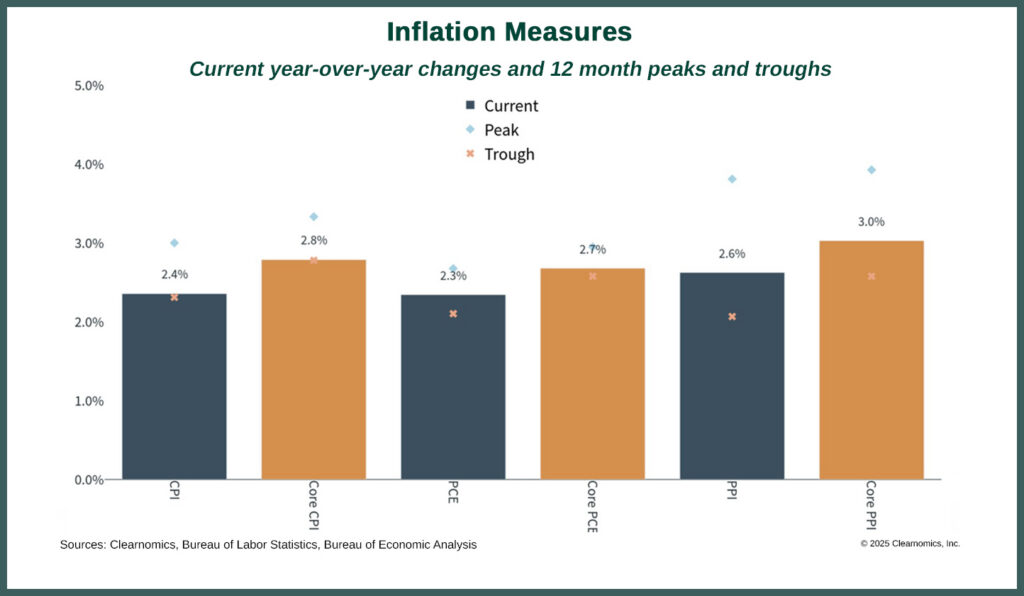

With the objective of keeping inflation low, this Federal Reserve has also been keeping interest rates high. Doing so gives the Federal Reserve more stimulus to support the economy during bear markets and recessions and also artificially inflates the rate at which banks borrow money. It’s worth noting that inflation has hung on to an acceptable 3% increase for the last three years (a point above the Fed’s self-imposed and somewhat arbitrary 2% goal) with no change of interest rates in sight.

The Federal Reserve is clearly affecting lending rates, which are a critical factor limiting economic growth. We know this because during Q1 2025, product (GDP) came in a negative run rate of -0.7% for Q1 2025. Although trade agreements did impact this reading, a negative number is never positive.

This policy is directly limiting the purchasing power of many Americans, preventing them from fully participating in the economy, which is clearly bad for everyone. Borrowers are experiencing higher interest rates for large purchases like homes, cars, and appliances, and these rates become even higher for consumers with lower incomes. This starts a domino effect for consumers and the economy alike. With more money being allocated towards just paying interest, less money is available to purchase goods, thus pulling money out of the economy and increasing the percentage of people who are living paycheck to paycheck. The formula for economic growth does not require all parties to continue to participate, but growth exceeds when all parties do.

A modest change in interest rates at the Federal level can change the game for borrowers

It could be argued that since the COVID-19 pandemic, the Federal Reserve has acted like the only adult in the room. While the Federal Government continued to deficit spend, between $1.3 and $3.1 trillion per year from 2020 to present, the Federal Reserve was more cautious, decreasing their balance sheet by trillions of dollars from 2021 to the present. The Fed has been exhibiting the age-old wisdom of “saving for a rainy day,” and it has worked.

Personal Consumption Expenditures, the Federal Reserve’s favorite measurement of inflation, has fallen to 2.3% from its highs of 7.2% in June of 2022. Over a similar time frame, the unemployment rate decreased from 14.7% in April 2020 to 4.2% as of April 2025.

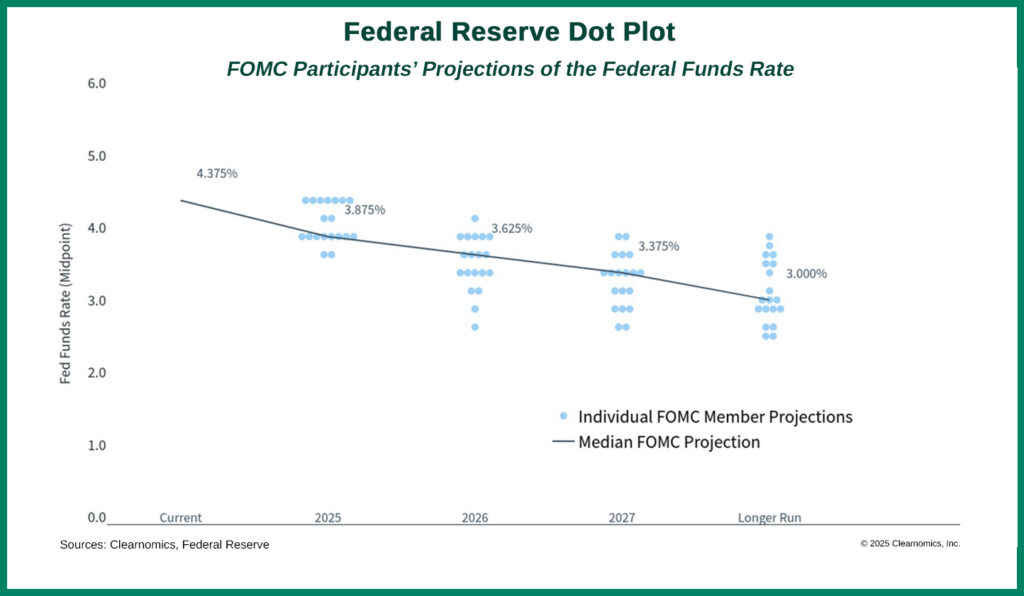

These numbers tell us that the Fed is fulfilling its mandate to keep inflation low and employment full and has been accomplishing this for years. So how can they alter their policy to help more Americans to participate in the economy: Should they keep rates at current levels until it breaks the economy? Or should they take action to normalize the economy by letting interest rates move down from their historical levels, easing the burden for the Federal Reserve to continue to increase interest rates to combat inflation?

We do not believe there is a need to be hasty and move interest rates from 4.2% down to 0%. A more modest reduction of 1% would help normalize borrowing rates across the board. Mortgage rates, for example, would likely decline about 5-10%. That’s a substantial material impact for borrowers.

We are also hoping that trade agreements will yield positive economic momentum, but we also continue to see a market that lacks confidence as the government waffles between policies promising austerity and/or trillion-dollar deficit spending. This uncertainty makes it near impossible for corporations to confidently hire employees or spend money on capital improvements such as new factories or machines. At the same time, the Federal Reserve seems terrified of lowering interest rates even when inflation and the unemployment rate has been at their target for three years and counting.

Indecisiveness kills and finance is not immune. As long as the Federal Government and Federal Reserve continue to increase uncertainty in the market, these institutions which are meant to provide stability and stimulus to our markets will continue to pull aggressively, but thankfully, not disproportionately, on one side of the proverbial rope.

The market is cheering for strong consumers and accelerating corporate profits

Despite this volatility, negativity is not winning the fight. The strength of the consumer and accelerating corporate profit growth has the S&P 500 returned to all-time highs. The consumer stood firm, with spending up 4.7% year-over-year, supported by real income gains and a robust job market. Corporate America also stood strong, with the S&P 500 earnings up 11.08%, driven by productivity and margin growth. Acknowledging the consumer’s financial strengths and corporate America’s accelerating profits has helped offset the stock market’s decline.

Consumer health is still a robust anchor

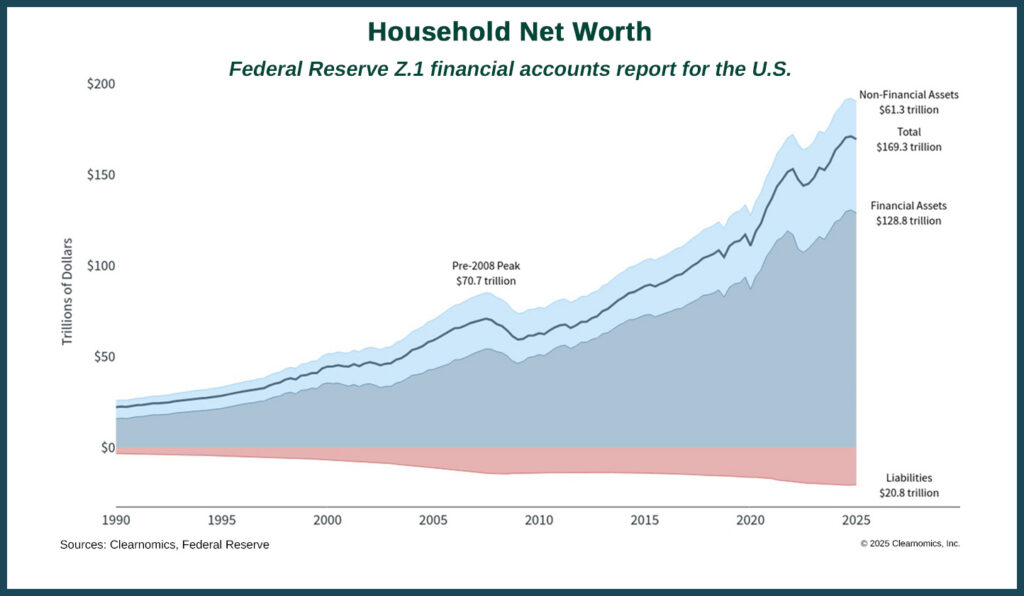

In the USA, consumers anchor the economy and today, the Consumer as a whole is still healthy. Holistically, household net worth is up 5% since early 2024 and was last measured in 1st Quarter of 2025 at a staggering $169 trillion.

Not only do we, as consumers, have wealth in the USA, our wages have been outgrowing inflation for three years. Typically, a healthy consumer is paired with a healthy job market, which we also have. There are currently 1.1 jobs open per unemployed individual looking for work — the job market has expanded dramatically from the 14.7% unemployment we saw in April 2020.

Corporate profits are pulling hard, too

Corporate Profits are also buoying the impact of a strong consumer on the market. In a typical bull market, profits grow by 7-8% per year, and history shows us that stock market performance follows profit growth. Even with uncertainty from both the Federal Government and the Federal Reserve, 1st quarter 2025 profits for the S&P 500 came in at 13%. This is a white-hot performance by any measure. Analysts are undeterred by the ongoing trade conversations and expect corporate profits to grow by 13-15% over the next 12 months.

A healthy consumer pairs very well with growing corporate profits in driving growth. Their relationship can act as a flywheel, where consumer spending fuels corporate profit growth which in turn provides the capital for wage increases above inflation. The two are a tough team to beat, economically speaking.

The Greenup Approach to Volatility: Opportunistic Risk Management

As a management team, we view market turbulence as an opportunity rather than a threat, and our approach to volatility is systematic and disciplined. We position our portfolios accordingly, accommodating a flat or declining stock market (up to 10% from its highest value) once a year. When this type of quick market movement occurs, it is generally guided by fear, which believe it or not, fear can be measured. When these fear indicators hit predefined thresholds, GreenUp will strategically analyze your risk and opportunistically increase risk in the portfolio, adding exposure to high-quality equities to capture rebounds.

A case in point: in Q2, as Liberation Day tariffs and fiscal uncertainty drove the market to its lows, our fear indicators flashed oversold, prompting us to incrementally increase stock exposure, particularly in consumer discretionary and technology sectors. This move, executed at the trough, allowed us to avoid managing in fear and instead act opportunistically, positioning your portfolio for gains as the market stabilized. Moving forward, we will continue to monitor these indicators, ready to add risk when fear peaks, ensuring your portfolio thrives amid volatility.

Conclusion: Holding Firm with Opportunistic Grit

As we continue to navigate the tug-of-war between economic forces in this dynamic market landscape, GreenUp remains steadfastly positioned to seize opportunities amid the volatility. The interplay of inflationary pressures, monetary policy shifts, and trade uncertainties, coupled with resilient consumer spending and corporate adaptability, defines the current environment. However, we are well-resourced to balance these competing forces. We view market fluctuations not as obstacles, but as chances to optimize portfolios and enhance client outcomes. Our team stands ready to proactively manage risks, capitalize on growth potential, and ensure your investments thrive, even as this tug-of-war continues to shape the financial horizon.

Executive Summary

- As we conclude the second quarter of 2025, financial markets remain engaged in a fierce tug-of-war.

- Fiscal policy, monetary policy, and trade uncertainty are exerting destabilizing pressure, driven by a shift toward deficit spending.

- The Federal Reserve is intent upon maintaining elevated interest rates, while disruptive “Liberation Day” tariffs continue to cause confusion in the markets.

- Meanwhile, consumer strength and corporate earnings are providing some stability, supported by resilient spending, rising profit margins, and strong productivity.

- Despite a volatile quarter characterized by negative GDP growth and low inflation, the S&P 500 achieved a 5.0% gain, though it experienced a 13.9% correction from all-time highs.

GreenUp Portfolio Updates

Dynamic, Index, and ESG Asset Allocation Portfolios

Target Risk of Benchmark: 105%

Target Risks: Changes

Sold FFSAX (Touchstone Flexible Income Fund Class A) and replaced with PIPNX Pimco Income Fund) (Dynamic and ESG models only)

Sold IJH (iShares Core S&P Mid-Cap ETF) and replaced with VO (Vanguard Mid-Cap ETF)

Sold IJJ (iShares S&P MidCap 400 Value ETF) and replaced with VOE

Sold IVOG (iShares S&P Small-Cap 600 Growth ETF) and replaced with VOT (Vanguard Mid-Cap Growth ETF)(Vanguard Mid-Cap Value ETF)

Target Risks: Large Cap Stock Model

Sells: ORCL (Oracle Corporation), VST (Vistra Corp), UNH (UnitedHealth Group Incorporated), OCOM (Omnicom Group Inc.), SLB (Schlumberger Limited)

Buys: ADBE (Adobe Inc.), AAPL (Apple Inc.), FSLR (First Solar Inc.), SNY (Sanofi), BRK.B (Berkshire Hathaway Inc. Class B), CRM (Salesforce Inc.), OMC (Omnicom Group Inc.), MA (Mastercard Incorporated), CMCSA (Comcast Corporation)

Equity Income Model

No Net Change: All other holdings remain at current weights

Tactical Equity Model

No Net Change: All other holdings remain at current weights

Tactical Income Model

No changes

Past performance is not indicative of future results. The material above has been provided for informational purposes only and is not intended as legal or investment advice or a recommendation of any particular security or strategy. The investment strategy and themes discussed herein may be unsuitable for investors depending on their specific investment objectives and financial situation. Information obtained from third-party sources is believed to be reliable though its accuracy is not guaranteed, and GreenUp makes no representation or warranty as to the accuracy or completeness of the information, which should not be used as the basis of any investment decision. Information contained on third party websites that GreenUp may link to are not reviewed in their entirety for accuracy and GreenUp assumes no liability for the information contained on these websites. Opinions expressed in this commentary reflect subjective judgments of the author based on conditions at the time of writing and are subject to change without notice. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission from Firm. For more information about GreenUp including our Form ADV brochures, please visit https://adviserinfo.sec.gov

Author

Daniel Greulich, CFA CFP®

Chief Investment Officer | Wealth Advisor | Ann Arbor, MI -- Daniel leads our Investment Committee and partners with Aaron Kirsch, Chief Client Advocacy Officer to design and implement client portfolios with your advisor. Daniel brings 14 years of practical experience as a trader, financial advisor, and money manager at both large and mid-sized financial services companies to GreenUp Wealth Management. In addition, he holds a CFP® designation and is also a CFA charterholder. This combination of experience and knowledge helps Dan confidently guide his clients through the development, execution and monitoring of their customized financial plans.

All Posts