Quarterly Market Update 2026 Q1

April 14, 2026 | Market Updates

As we enter the second quarter of 2026, geopolitical conflict and market volatility are commanding investor attention and stoking real fear. That fear has a way of collapsing complexity, making the economy feel simpler – and darker – than it really is.

Beyond the Outer Layer: Uncovering the Core Strength of 2026

As we enter the second quarter of 2026, geopolitical conflict and market volatility are commanding investor attention and stoking real fear. That fear has a way of collapsing complexity, making the economy feel simpler – and darker – than it really is.

The reality of today’s economy is far more nuanced. Rather than a single, undifferentiated story, the economy is better understood as layers within layers, similar to a Russian Matryoshka doll, where surface conditions obscure a fuller picture that only emerges on closer examination. Right now, three distinct layers define that picture:

- Geopolitical Tension: Conflict risk involving Iran – impacting oil prices and compounded by continued Federal deficit spending.

- Monetary Shifts: A Federal Reserve leadership transition and evolving interest rate policy.

- Fundamental Health: Record uncertainty set against strong corporate earnings and a resilient labor market.

These layers are not isolated; they are interrelated. Much of today’s investor anxiety comes from fixating on the outermost one and projecting a single outcome: recession. But contraction is not the only story these conditions can tell. At GreenUp Wealth, we believe peeling back the layers reveals a path toward growth, not away from it.

The Outer Layer: Geopolitical Tension & Fiscal Policy

The outermost layer, which is setting the tone for everything else beneath it, is the tension between the U.S. and Iran. And, right now, that tone is inflationary.

Economists have a substantial historical record to draw from when it comes to war and economic outcomes. The pattern is consistent: military conflict can generate a short-term stimulus through increased government spending, but wartime production is ultimately a net negative. Single-use munitions, destroyed infrastructure, idled factories — these represent a deeply inefficient use of capital. Productive assets are consumed rather than built, and the long-run cost is measured in inflation, not growth. The humanitarian toll, of course, sits in a category of its own.

This inflationary pressure doesn’t arrive in isolation. U.S. consumers are currently receiving a meaningful fiscal stimulus through the 2025 tax season, embedded in the Federal budget. Increased standard deductions, enhanced deductions for seniors over 65, and adjusted tax brackets amount to what might be called “tax Easter eggs:” targeted relief that puts real money back into household budgets. Unlike wartime expenditure, this form of spending is relatively efficient. But it is still deficit spending, and it adds another layer to an already familiar story.

In the near term, this liquidity will likely support consumer activity and keep recession off the immediate horizon. The longer-term implication, however, points toward inflation that proves stubborn — slow to ease, resistant to quick fixes. While the combination of wartime expenditures and increased tax deductions may not catapult the Consumer Price Index back to the 9.1% peak seen in 2022, it is likely to anchor inflation near 4%. This significantly overshoots the Federal Reserve’s 2% target for a sustained period, creating the common thread that connects this outer layer to the economic realities nested beneath it.

The Middle Layer: Monetary Policy & The Resilient Consumer

If Federal deficit spending has been a driver of inflation, then the Federal Reserve’s mandate is to contain it. That tension brings us to the second layer: the Fed and the American consumer.

May is shaping up to be a pivotal month. Jerome Powell’s term concludes, and Kevin Warsh is set to succeed him. It is a transition that, on its surface, is simply one capable economist handing the reins to another. But leadership changes at an institution like the Fed are rarely just administrative. Both men are highly competent, yet they represent meaningfully different philosophies about how the world’s most influential central bank should operate. That difference matters because of what the Fed controls.

Interest rates are not merely a technical lever. They shape how consumers borrow, spend, and plan. And consumer behavior, in turn, drives roughly 70% of U.S. economic growth. When the Fed shifts its posture, the effects move through the entire economy, layer by layer. How Warsh chooses to navigate the inherited tension between growth and inflation will set the tone for much of what follows.

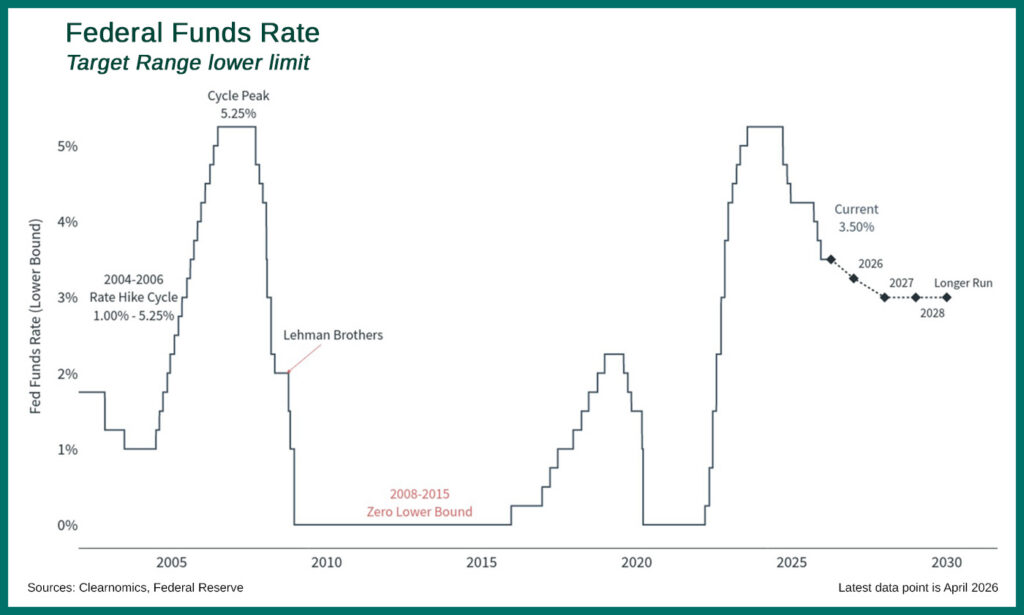

The Powell Era: The Interest Rate “Hammer”

To understand where the Fed is headed, it helps to understand the tool Jerome Powell relied on most and how heavily he used it.

Powell’s tenure was defined, above all, by the Federal Funds Rate. In response to post-pandemic inflation, the Fed embarked on one of the most aggressive tightening cycles in modern memory, lifting rates from a near-zero floor of 0%–0.25% all the way to a peak range of 5.25%–5.50%. The logic was straightforward, but blunt: make borrowing more expensive, cool demand, and bring prices back under control. Homebuyers felt it.

Corporations felt it. The cost to borrow money became the dominant force shaping economic behavior across the board.

By 2025, the pressure had begun to work. As inflationary signals stabilized, the Fed initiated a measured series of cuts, bringing the rate down to 3.5% by early 2026. The blunt force worked.

What Powell leaves behind is an economy shaped by what might be called “interest rate dominance” — an era in which the price of borrowing was the primary instrument of stability. It was effective at accomplishing the stated objective, but it was also a hammer. The question worth sitting with, as leadership changes hands, is whether the challenges ahead call for the same tool or a different one entirely.

The Warsh Outlook: A Strategic Pivot to the Balance Sheet

While Powell focused on the cost of money, the market anticipates that Kevin Warsh will focus on the quantity of money. As he prepares to take the helm, we can expect lower interest rates, possibly below their current 3% target. The more accommodative interest rate environment should provide much-needed breathing room for small businesses and families who depend on borrowing money for liquidity and growth.

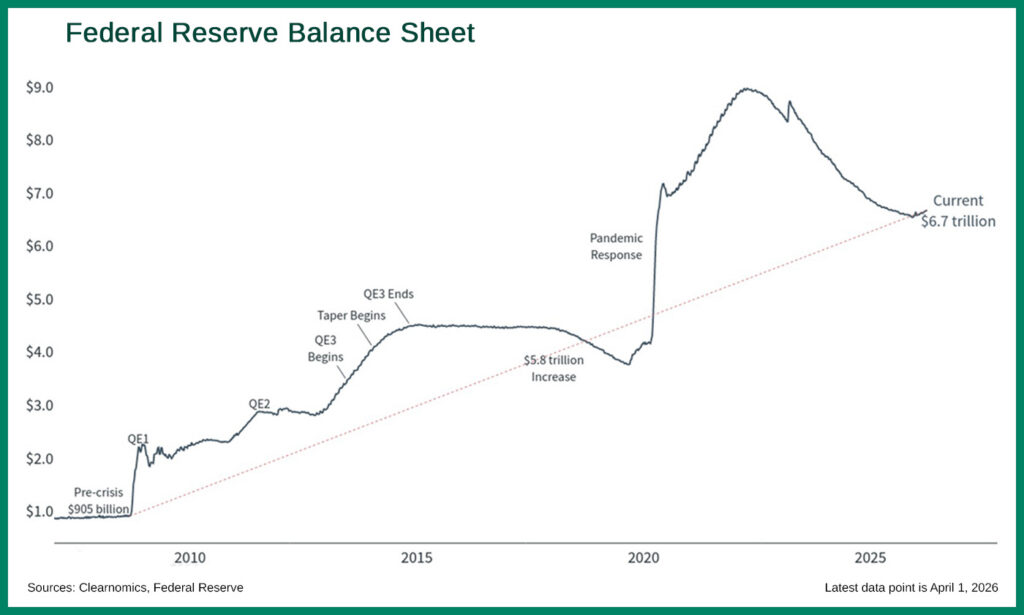

However, to ensure this doesn’t reignite inflation, Warsh is expected to pivot the Fed’s focus toward Quantitative Tightening (QT). This involves aggressively shrinking the Federal Reserve’s massive $7 trillion balance sheet, which, while down from its $9 trillion peak, remains historically elevated. By selling off these assets, the Fed removes liquidity from the financial system, effectively pulling excess dollars out of the economy. In short, the strategy moves from high borrowing costs to a reduced money supply, aiming for a “soft landing” that supports growth while keeping a lid on prices.

The Result: A Resilient but Friction-Filled Consumer

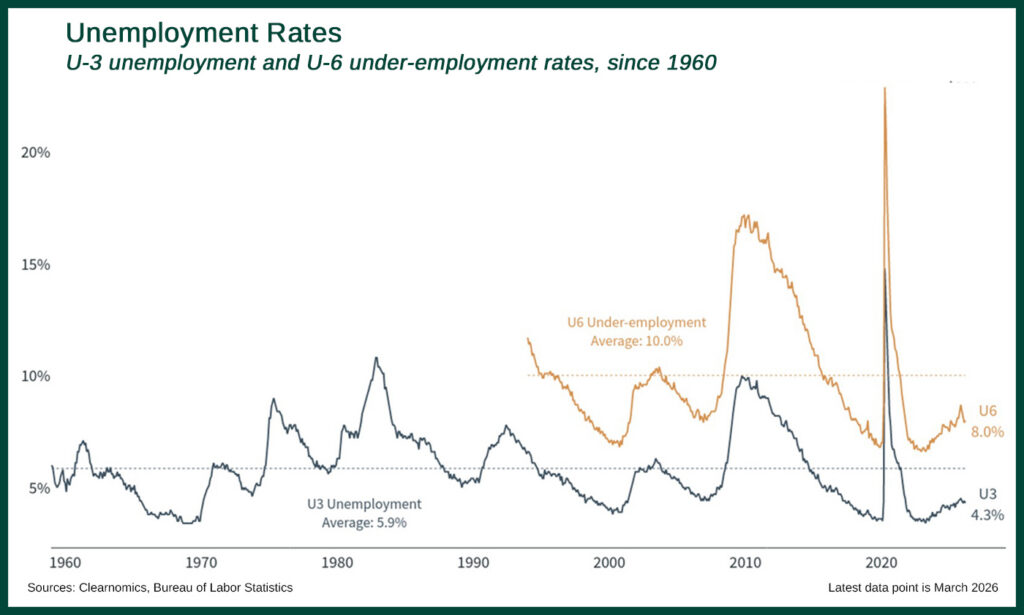

By shifting the burden away from interest rates and toward the balance sheet, this new strategy could provide a short-term stimulus to a consumer who is remarkably robust yet increasingly weary. Currently, the American labor market remains structurally sound; as of January 2026, unemployment stands at 4.3% with 6.9 million job openings – a far cry from the 9.9% peak of the Great Recession.

Despite this employment strength, significant friction exists. The modern consumer is navigating the dual pressures of persistent inflation and the lingering weight of elevated debt costs. While the Fed’s new direction offers a glimmer of relief, the stakes remain high: if consumer spending begins to stall under these pressures, the stability of corporate profits will be the next layer of the economy to face scrutiny.

The Inner Core: Corporate Health vs. The “Fog of War”

In 2026, the sheer volume of information has created a “fog of war” that obscures fundamental data. The innermost “Russian doll” reveals the truth about current risk tolerance.

The Economic Policy Uncertainty Index is currently at an all-time high, reaching levels comparable to the 2008 financial crisis. However, this spike is largely driven by the polarization and volume of media coverage rather than a fundamental economic breakdown. With the advent of the internet and the digital age, the term “the news” has taken on many different meanings; defining news anchors and independent journalists in the same breath and often in the same terms. The “news” media seemingly changed their goals from accuracy to speed over the last two decades. Now, the “news” can often be the primary source of uncertainty, not the underlying economy.

In stark contrast to this media-driven anxiety, Corporate America continues to report double-digit earnings growth. Our forecast for the next 12 months is 12.5% earnings growth, with expectations for the next three years remaining strong. When you pair healthy consumer spending with increased productivity, driven by the evolution of AI, the equation remains positive. Strong earnings ultimately lead to strong investment performance.

The Core of the Matter: Strategy Over Sentiment

As we peel back the layers of 2026, it becomes clear that while the outer layer of the “Russian dolls” of geopolitics and fiscal policy are imposing, they do not tell the whole story. The “inner-most doll” reveals a landscape defined by fundamental resilience rather than impending collapse. While the fog of war and the friction of sticky inflation are real risks, they are balanced by a pro-growth Federal Reserve transition, a resilient consumer and a private sector that continues to outpace expectations through productivity and earnings.

At GreenUp Wealth Management, we aren’t simply watching these layers reveal themselves — we are actively positioning your investments to meet what’s inside. Our strategic response to this nested economy focuses on three key areas:

- Selectivity and Flight to Quality: We are strategically rotating portions of fixed-income allocations from corporate bonds into government bonds. We believe sovereign credibility remains the ultimate refuge during geopolitical shifts.

- Active Exposure Management: To account for late-cycle expansion and potential volatility, we have modestly reduced overall equity exposure. This creates a “volatility buffer,” ensuring your portfolio isn’t over-extended if the headlines turn sharp.

- Concentrated Growth: Our focus remains on large-cap growth and emerging markets. These sectors currently offer the highest fundamental strength and the best margin protection through AI-led productivity.

Investing successfully requires the discipline to look past the outer narrative of fear and focus on the structural health at the core. We encourage you to reach out to your GreenUp Wealth Advisor to review your financial plan and risk tolerance to ensure your plan is aligned with these underlying drivers of growth. Together, we will stay rooted in what the layers tell us, undistracted by the noise, and positioned for what lies ahead.

GreenUp Portfolio Updates

Dynamic/ESG Models: New Positions: Vanguard Short-Term Bond ETF (BSV)

Exited Positions: iShares 0-5 Year Investment Grade Corporate Bond ETF (SLQD)

Equity Income Model New Positions: Brookfield Asset Management Ltd. (BAM)

Exited Positions: Omnicom Group, Inc. (OMC)

Large Cap Stock Model New Positions: (AVGO), Booking Holdings, Inc. (BKNG), Eli Lilly & Co. (LLY), Valero Energy Corp. (VLO), Credo Technology Group (CRDO), Autodesk, Inc. (ADSK) Exited Positions: Check Point Software (CHKP), Comcast Corp. (CMCSA), Adobe, Inc. (ADBE), Salesforce, Inc. (CRM), Air Products & Chemicals (APD), Omnicom Group (OMC), The Walt Disney Co. (DIS), DexCom, Inc. (DXCM)

Tactical Equity Model New Position: First Trust Large Cap Value Opportunities AlphaDEX Fund (FTA), First Trust Energy AlphaDEX Fund (FXN)

Exited Position: First Trust Large Cap Value Opportunities AlphaDEX Fund (FTC), SPDR S&P 500 ETF Trust (SPY)

GreenUp Street Wealth Management, LLC d/b/a GreenUp Wealth Management is an investment advisory firm registered with the Securities and Exchange Commission (“SEC”) under the Investment Advisers Act of 1940. Registration as an investment adviser does not imply a certain level of skill or training. The oral and written communications of an adviser provide you with information about which you determine to hire or retain an adviser. Form ADV Part 2A can be obtained by visiting https://adviserinfo.sec.gov and searching for our firm name. ADV Form 2B is available upon request. Neither the information nor any opinion expressed is to be construed as solicitation to buy or sell a security or personalized investment, tax, or legal advice.

This report has been provided for informational purposes only and is not intended as legal or investment advice or a recommendation of any particular security or strategy. The investment strategy and themes discussed herein may be unsuitable for investors depending on their specific investment objectives and financial situation. Information obtained from third-party sources is believed to be reliable though its accuracy is not guaranteed. Opinions expressed in this commentary reflect subjective judgments of the author based on conditions at the time of publication and are subject to change without notice. Past performance is not indicative of future results.

Any forecasts presented in this document, including estimates of returns or performance, are “forward looking statements”, are based upon certain assumptions about future events or conditions and are intended only to illustrate hypothetical results under those assumptions, and no assurances can be made that they will materialize. Forward-looking statements are based on an assumption that economic, market, political, operational, legal, tax, regulatory and other conditions will not deteriorate and, in some cases, improve.

Author

Daniel Greulich, CFA CFP®

Chief Investment Officer | Wealth Advisor | Ann Arbor, MI -- Daniel leads our Investment Committee and partners with Aaron Kirsch, Chief Client Advocacy Officer to design and implement client portfolios with your advisor. Daniel brings 14 years of practical experience as a trader, financial advisor, and money manager at both large and mid-sized financial services companies to GreenUp Wealth Management. In addition, he holds a CFP® designation and is also a CFA charterholder. This combination of experience and knowledge helps Dan confidently guide his clients through the development, execution and monitoring of their customized financial plans.

All Posts