Quarterly Market Commentary: Priced to Perfection

October 8, 2024 | Market Updates

GreenUp Wealth Management reviews Q3-Q4 2024 market conditions, high valuations, Fed policy, corporate earnings, consumer strength, and portfolio strategy.

As we enter into the final quarter of 2024, I’m intrigued by how human psychology affects financial markets. How do our emotions, particularly excitement about future gains, influence our investment decisions and ultimately the market itself? Are our expectations aligned with reality, and what is the impact of those expectations?

When I think of expectations aligning with reality, I think of Doughnut Day at my house every Sunday morning. My daughters choose their ideal doughnut the night before: chocolate cake with chocolate icing for Lily, and a pink-frosted doughnut with sprinkles for Penelope. Their excitement lasts through the night, and they run downstairs the next morning eager to find their chosen doughnuts waiting on the table.

However, there are times when their preferred choices aren’t available, and my wife and I have to find alternatives. What happens if they find chocolate instead of pink icing, no sprinkles, or a plain glazed doughnut? Instead of focusing on the fact that they get delicious doughnuts for breakfast, they focus on how their expectations were different from reality.

There are parallels between the current market environment and Doughnut Day. Expectations are particularly important this quarter, because the current market is both promising and inherently precarious, precisely because expectations are out of line with reality. The S&P 500 is up 22%, almost every asset has resulted in a positive return for 2024, and conversations around a hard landing for the economy have seemingly come and gone. The good times are here to stay, right? The answer is yes and no because the market reacts to both cold hard facts and individuals’ opinions on how those facts will affect the economy. Unfortunately, opinions can be wrong.

Some analysts describe this market as “priced to perfection,” meaning the fundamentals of the economy are solid and thus stock prices are high. However, this sentiment can change quickly with negative news, leading to an overreaction. Despite the potential volatility, our market is fundamentally strong.

“Irrational exuberance” is a phrase suggesting that the stock market is overvalued. With so much positive news floating around, the market is acting like an irrational “child” – prone to overreacting to the positive side. But as we all know, sentiment can shift quickly. There’s very little room for negative surprises in a market of this exuberance. Any unexpected economic data, shifts in Federal Reserve policy, or geopolitical tensions could trigger a revaluation, leading to significant downside risk.

For now, the stock market continues to push forward, buoyed by expectations of lower interest rates, strong corporate earnings, and a steady consumer (the exact formula we look for in an expanding economy). We expect this positive economic environment to stay with us through 2027. If the stock market was rational, we would not have a problem. The phrase “priced to perfection” has become a fitting description of today’s market, and the underlying tone of optimism is not misplaced. As we move through the final quarter of 2024, it is clear that optimism in the financial markets has returned, even if current expectations are a bit unrealistic.

At GreenUp, we recognize that in markets with high expectations, any hint of uncertainty can send ripples through the system. Disciplined, measured approaches are key, especially when optimism is high and risks, such as changes in the Fed’s interest rate policies, lower-than-expected corporate earnings, and decreased consumer spending, may be bubbling just beneath the surface. In this Quarterly Market Update, we’ll take you through why we see clear opportunities and reasons to participate in the financial markets—but also why a cautious outlook is prudent as we head into the final months of the year.

Monetary Policy is Always a Balancing Act

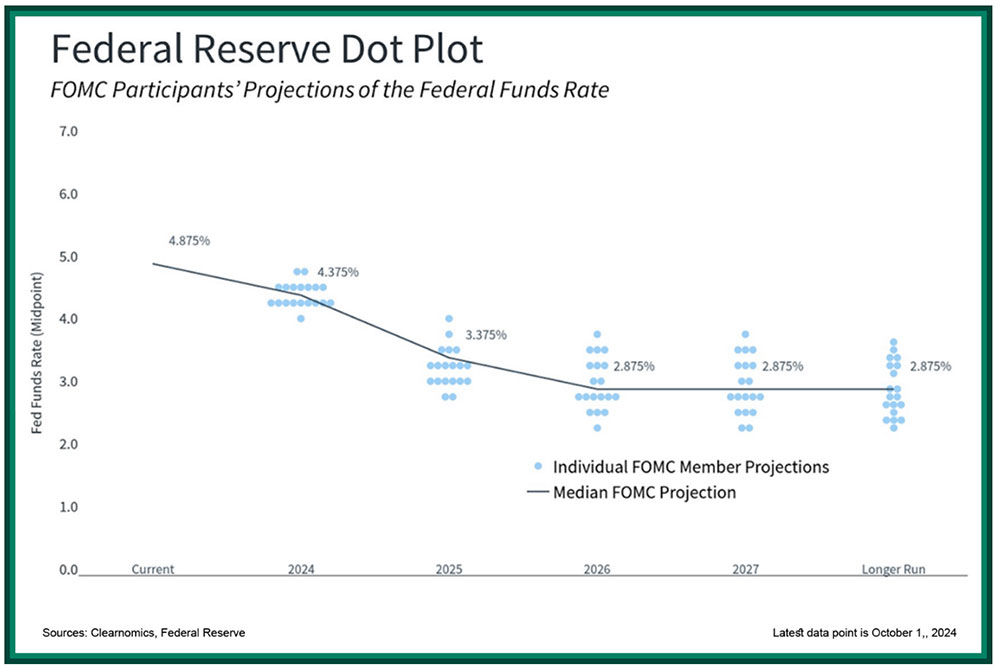

Inflation has been persistent since 2022, but as we turn towards 2025, the Federal Reserve is beginning to ease its grip on the financial market. The market has taken this as a sign of future growth, with interest rates expected to slowly decline after reaching their peak earlier this year. Lending costs should continue to decrease for the next couple of years, which is fantastic

news. But whether this decrease will happen quickly enough to boost the market is an open question. While the Federal Reserve has signaled that rate cuts will be gradual, the market seems to be betting on a faster decline. This discrepancy in expectations may not lead to a negative market at the end of the day, but it will introduce periods of volatility where market expectations may have to adjust to reality.

Lower interest rates will create a more favorable borrowing environment for businesses and homeowners alike. Of course, there is a catch. If the economy grows too quickly and thus aggravates inflation, the Federal Reserve may have to pause or even reverse its interest rate cuts. This will slash market expectations. As we can see, setting interest rates is a delicate balancing act, and the market’s priced-in assumptions leave little room for any missteps.

Corporate Earnings Are Still Growing, Just Slower

There’s no doubt that corporate earnings have been strong. There’s a lot of hope baked into current valuations, especially as S&P 500 companies report earnings growth and provide optimistic projections for 2025. The forward price-to-earnings ratio (which is calculated using forecasted earnings) for the S&P 500 is above its historical average, signaling confidence—but also risk. Just as with interest rate cuts, this positive environment is expected to continue into 2027.

If earnings fall short of the market expectations, we could see a normal correction in stock prices. In fact, the scenario is similar to our current predicament with interest rates – the market expectation is ahead of reality. Because of the strength and staying power of corporate earnings, any decrease should be regained in the following months as the growth expectation for stocks is not solely saddled in 2025. Mid-teens earnings growth is expected through 2027 which should give the market an upward trajectory.

There are many economic bright spots. More asset classes have healed in the past year than deteriorated. For example, Mid and Small Cap stocks have seen a return to positive growth expectations. These asset classes are inexpensive compared to Large Cap stocks and offer a double-digit growth potential, making an argument for investors to allocate more of their dollars into Mid and Small Cap. The type of growth we are seeing in earnings is reminiscent of a mid to early-cycle bull market, which historically lasts five to six years.

How Long Can Consumers Keep It Up?

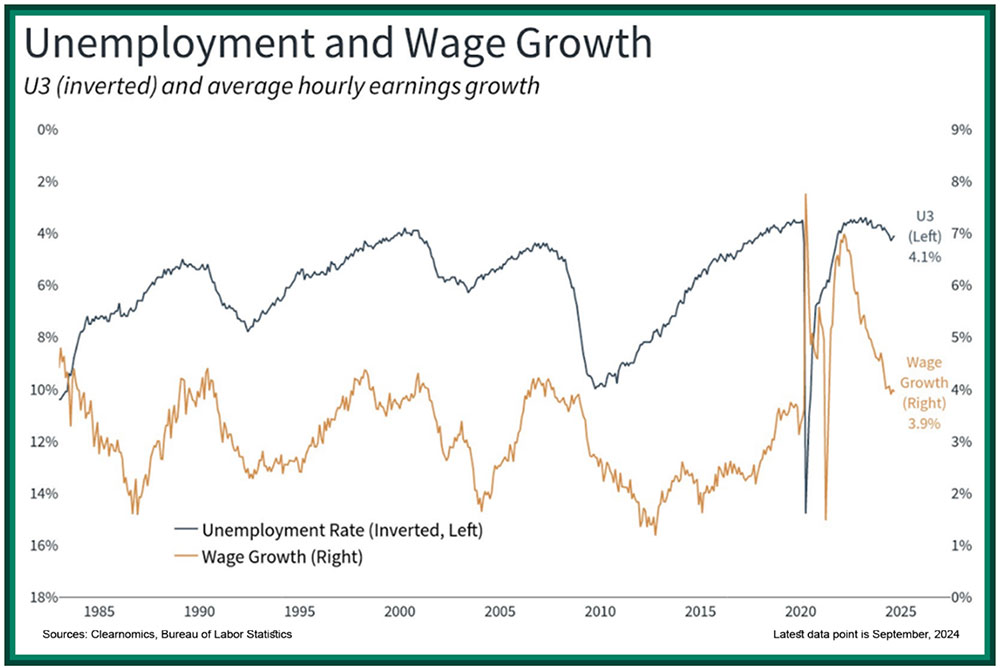

The American consumer remains resilient. Anytime we see the cost-of-living increase (which has been approximately 20% over 36 months), one has to be concerned about the health of the consumer. But wage growth remains solid, and wages are increasing faster than inflation. Meanwhile, the job market has one million more jobs than individuals looking for jobs. In the long term, these are positive trends for the US economy. For now, the overall picture remains one of a consumer base that is holding strong.

However, in the near term, the job market is exhibiting some signs of slowing. Unemployment is holding steady at 4.1%, which is an increase from 3.8% in September 2023. Pairing this with flat-to-decelerating consumer spending, Main Street’s duress is legitimate. These are subtle but important signals that the economy’s engine—consumer spending—might be starting to cool.

The Federal Reserve acknowledges this stress. Although most of our commentary focuses on corporations, a decrease in lending rates will be a positive catalyst for consumers as a whole. What we know is that a healthy consumer is imperative to our investment thesis through 2025, and will be critical in shaping the economic landscape and performance of the market.

The stock market continues to push forward, buoyed by expectations of lower interest rates and strong corporate earnings. But as we all know, sentiment can shift quickly. With valuations stretched and the market “priced to perfection,” there’s very little room for negative surprises. Any unexpected economic data, a shift in Federal Reserve policy, or geopolitical tensions could trigger a revaluation, leading to significant downside risk.

Conclusion: A Measured Approach

As we look towards the end of 2024 and into the new year, it’s important to recognize both the opportunities and the risks inherent in today’s market. At GreenUp, we advocate for a cautious but optimistic approach. It’s easy to get swept up in the positive momentum, but it’s important to remain grounded in fundamentals. Diversification, careful sector selection, and an eye on risk management will be critical as we navigate the months ahead. Our approach will continue to focus on finding value where it exists while managing downside risk.

Bonds still offer some protection in a volatile environment. Equities will likely outpace bonds in performance, but we will remain selective in our exposure, particularly in sectors where growth remains strong and valuations are more reasonable. In these times, the key is not to chase every rally but to stay disciplined, diversified, and prepared for whatever the market throws at us next.

GreenUp Portfolio Updates

Dynamic Portfolios

We are increasing our equity exposure to iShares S&P 500 Value ETF (IVE), iShares Core S&P 500 ETF (IVV), Avantis Emerging Markets Equity ETF (AVEM), and iShares S&P Mid-Cap 400 Value ETF (IJJ) and decreasing our exposure to Invesco QQQ Trust (QQQ), Health Care Select Sector SPDR ETF (XLV), and Avantis US Small Cap Value (AVUV).

We are increasing our fixed income exposure to iShares 20+ Year Treasury ETF (TLT) and iShares 0-5 Year Investment Grade Corp Bond ETF (SLQD) and decreasing our exposure to iShares Core US Aggregate Bond ETF (AGG) due to uncertainty around future interest rate movements.

Large Cap Stock Model

We added Taiwan Semiconductor Manufacturing Co Ltd (TSM), Boston Scientific Corp (BSX), and Qualcomm Inc (QCOM). We removed Novartis AG (NVS), Autodesk Inc (ADSK), Salesforce Inc (CRM), and Lockheed Martin Corp (LMT) from the portfolio.

Equity Income Model

We removed Airbus SE (EADSY) due to the company not increasing its dividend yield in line with price increases.

Tactical Equity Model

We sold iShares MSCI EAFE ETF (EFA), iShares S&P Mid-Cap 400 Growth ETF (IJK), and Invesco QQQ Trust (QQQ) and added iShares US Real Estate ETF (IYR), iShares S&P 500 Value ETF (IVE), and SPDR Dow Jones Industrial Average ETF (DIA).

Tactical Income Model

We sold VanEck High Yield Muni ETF (HYD) and iShares iBoxx High Yield Corp Bond ETF (HYG) and added iShares 20+ Year Treasury ETF (TLT) and iShares iBoxx Investment Grade Corporate Bond ETF (LQD).

Past performance is not indicative of future results. The material above has been provided for informational purposes only and is not intended as legal or investment advice or a recommendation of any particular security or strategy. The investment strategy and themes discussed herein may be unsuitable for investors depending on their specific investment objectives and financial situation. Information obtained from third-party sources is believed to be reliable though its accuracy is not guaranteed, and GreenUp makes no representation or warranty as to the accuracy or completeness of the information, which should not be used as the basis of any investment decision. Information contained on third party websites that GreenUp may link to are not reviewed in their entirety for accuracy and GreenUp assumes no liability for the information contained on these websites. Opinions expressed in this commentary reflect subjective judgments of the author based on conditions at the time of writing and are subject to change without notice. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission from Firm. For more information about GreenUp including our Form ADV brochures, please visit https://adviserinfo.sec.gov

Author

Daniel Greulich, CFA CFP®

Chief Investment Officer | Wealth Advisor | Ann Arbor, MI -- Daniel leads our Investment Committee and partners with Aaron Kirsch, Chief Client Advocacy Officer to design and implement client portfolios with your advisor. Daniel brings 14 years of practical experience as a trader, financial advisor, and money manager at both large and mid-sized financial services companies to GreenUp Wealth Management. In addition, he holds a CFP® designation and is also a CFA charterholder. This combination of experience and knowledge helps Dan confidently guide his clients through the development, execution and monitoring of their customized financial plans.

All Posts